On March 11, 2026, the European Central Bank (ECB) announced the Appia strategic roadmap, designed to establish a tokenized wholesale financial market ecosystem in Europe, backed by central bank money. Beyond being a technical upgrade, this initiative is the pillar of the strategy to build a European tokenized financial ecosystem.

Blockchain technology can make transactions faster, simpler and available 24/7. The Appia roadmap sets out how to integrate it within Europe’s financial system https://t.co/J46s6mCfQR pic.twitter.com/3jDdGgCJ1P

— European Central Bank (@ecb) March 11, 2026

It is essential to understand that this move transcends the simple modernization of infrastructures. The real backdrop of Appia is strategic and geopolitical: it is about ensuring that Europe’s next digital financial layer is sovereign. The goal is to prevent future markets from depending on external networks, standards, or actors, ensuring that the heart of the European financial system beats under its own rules.

«With Appia, we are building a path from the current financial system towards the tokenized markets of tomorrow, firmly based on central bank money,» said Piero Cipollone, member of the ECB’s Executive Board.

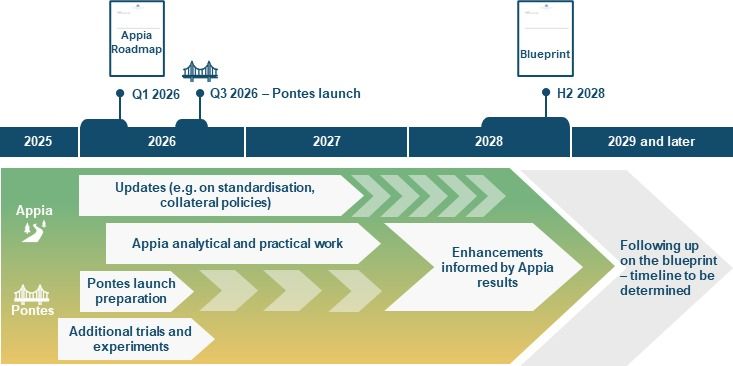

A key element of this initiative is Pontes, the Eurosystem’s distributed ledger technology (DLT)-based settlement solution from the ECB, which is expected to be operational by the third quarter of 2026. Pontes will be interoperable with the Eurosystem’s TARGET payment settlement services.

In conjunction with the roadmap’s launch, the ECB has initiated a public consultation to gather feedback from both the public and private sectors, with a deadline for responses on April 22. Additionally, the ECB plans to launch a digital euro pilot program in the second half of 2027, marking a significant step towards integrating digital currency into the European financial landscape.

Why is the ECB betting on tokenization now?

For the European Central Bank, tokenization is not an experiment with emerging technologies, but a defensive and offensive response to the new global financial order. The commitment to Appia and Pontes responds to a pragmatic reading of power: whoever controls the infrastructure, controls the rules of the game. Here are the three axes that explain why the ECB has moved from observation to direct action:

|

Strategic axis |

Risk of dependency |

Solution and benefit (Appia/Pontes) |

| 1. Strategic autonomy | Digital servitude: Depending on networks controlled by Big Tech or foreign powers, losing the ability to oversee one’s own financial flows. | Technological sovereignty: Ensuring that the settlement infrastructure is European, protecting data and avoiding external geopolitical pressures. |

| 2. Market competitiveness | Fragmentation and obsolescence: A divided European system losing relevance against the advance of the digital dollar or digital yuan. | Native integration: Ensuring that digital assets from the entire EU «speak the same language» (interoperability), creating a more attractive, faster, and programmable market. |

| 3. Central Bank money as an «Anchor» | Systemic instability: The market massively adopting private stablecoins without the backing or security of a public institution. | Stability and control: Keeping central bank money at the core of the DLT system, ensuring the transmission of monetary policy in the digital age. |

Appia and Pontes: the two pieces of the plan

To understand the ECB’s digital deployment, it is essential to see Appia and Pontes not as isolated projects, but as the two gears of the same engine.

- Appia is the strategic brain:the master plan defining what the entire European financial system will look like until 2028, ensuring Europe maintains its sovereignty and competitiveness.

- Pontes is the executing arm:the technical tool that will be ready much sooner (in 2026) for banks to start operating in the digital world with the security of central bank money.

|

Feature |

Appia (The master plan) |

Pontes (The tool) |

| Nature | Strategic: It is the roadmap and the long-term architectural design. | Operational: It is the immediate, functional technical solution (the DLT infrastructure). |

| Time horizon | Continuous design and coordination work until 2028. | Launch planned for the third quarter of 2026. |

| Main function | Define the rules, standards, and the role of the euro in a smart contract market. | Serve as a «bridge» to settle digital transactions today using current systems (TARGET). |

| Final objective | Achieve an integrated, autonomous, and competitive European financial ecosystem. | Allow the financial sector to operate now with the safest settlement asset that exists. |

| Relationship | It is the framework that will guide future improvements and the evolution of the system. | It is the first practical implementation that will eventually be integrated within Appia. |

In summary, while Appia designs the future, Pontes builds the bridge to reach it.

What is tokenization, and why does it change the rules?

Tokenization is not simply about «putting assets on a blockchain»; it is the redesign of financial «plumbing». It is about representing assets and rights on a programmable digital infrastructure (DLT networks) that allows integrating all stages of an asset’s life cycle on a single platform.

By using Smart Contracts, processes that previously required days and multiple intermediaries can now be automated, improving efficiency and enabling much more agile forms of exchange and settlement. However, for the ECB there is a non-negotiable premise: even if technology changes, central bank money must remain the anchor of trust that guarantees the stability of the entire system.

The Eurosystem articulates this transformation through two mutually reinforcing initiatives:

- Appia:Defines the roadmap for both the private and public sectors to develop tokenized services under a common framework.

- Pontes: Is the Eurosystem’s operational offering. While Appia designs the future, Pontes provides the practical infrastructure that will be gradually refined to execute these transactions.

To ground the ECB’s vision, it is essential to understand that this deployment seeks not only a technical improvement, but a reaffirmation of European financial sovereignty. Aligning infrastructure with global debates on competitiveness allows Europe to stop being a spectator and become the architect of its own payment network.

Below are the strategic and geopolitical objectives underpinning this paradigm shift:

|

Objective |

Description and scope |

Strategic impact |

| Elimination of fragmentation | Appia establishes shared DLT networks under common standards for the entire Eurosystem. | Reduces entry barriers and ensures that infrastructure does not depend on external networks or actors (Big Tech). |

| Operational efficiency | Native integration into digital platforms to simplify the relationship between financial institutions. | Drastic reduction in settlement times and operational costs of the system. |

| Resilience of the euro | Ensures that central bank money is the definitive settlement asset on DLT networks. | Guarantees that monetary policy remains effective and sovereign, keeping the euro as the anchor of trust. |

Is Europe arriving late or on time?

The answer requires a strategic and pragmatic reading, far from any unnecessary epic. The global scenario shows that actors like the United States, Switzerland, and Singapore are already deploying blockchain-based financial infrastructures. However, the ECB is not reacting to a fad, but to a window of opportunity that still remains open.

The real debate today is not whether tokenization will become the standard, but who will define the rules, the protocols, and above all, the reference assets that will circulate on those new networks.

|

Perspective |

Current situation |

Europe’s strategic objective |

| The global environment | Other actors are already experimenting with tokenized markets and private DLT infrastructures. | Avoid the «closed network» effect where standards are imposed by third parties. |

| The Time factor | Technology is maturing, but global standards are not yet consolidated. | Make a move now with Appia and Pontes to influence the financial architecture of the 21st century. |

| The definition of «Success» | It is not just about being the first to innovate technically. | It is about doing so before being trapped in foreign infrastructures and rules. |

Indeed, the European Central Bank is not presenting a simple technological demonstration, but a definitive political and technical direction for the coming years. By integrating the strategic vision of Appia with the operational capacity of Pontes, the ECB ensures that the euro and central bank money remain as the anchor of trust in a financial system that is becoming irremediably programmable, tokenized, and interoperable. This unified commitment seeks to ensure that Europe’s next digital layer is sovereign, preventing the standards and rules of the future from depending on external networks or actors that compromise the continent’s financial autonomy.