In 2025, the future of money is on everyone’s lips, and not just because of the cryptocurrencies you already know. The protagonist of this conversation is a concept that seeks to redefine money as we know it, merging digital technology with the central authority of the State: the CBDC or Central Bank Digital Currency.

Unlike decentralized assets like Bitcoin, a CBDC is your country’s money, but in digital format. It is not a promise of payment, nor a representation of money, it is the money itself, issued and controlled by the central bank. It is the governments’ response to the digital era, an attempt to modernize their financial systems and maintain monetary sovereignty in a world where money moves at the speed of light.

What is a CBDC?

A central bank digital currency, or CBDC for its acronym in English (Central Bank Digital Currency), is a new form of money issued electronically by a central bank. Central banks seek to issue their own digital currencies with the objective of improving the payment system, given the increase in electronic payments and the decline in the use of cash, but also because the creation of unregulated private electronic payment instruments can put financial stability at risk.

Unlike traditional cryptocurrencies like Bitcoin or Ethereum, CBDCs are backed by the government and have the same value as the physical money we already know, like bills and coins.

Don’t be confused: CBDCs are not cryptocurrencies

Although CBDCs and cryptocurrencies are digital and may use similar technologies like blockchain, their philosophies and purposes are opposite:

- Centralization. CBDCs are controlled by central banks, while cryptocurrencies are decentralized and do not depend on any authority.

- Stability. CBDCs have a fixed value backed by the official currency of a country, like the dollar or the euro. Cryptocurrencies can be very volatile, and their price varies according to supply and demand in the market.

- Objective. CBDCs seek to modernize financial systems and offer a safe and accessible form of digital money. Cryptocurrencies, on the other hand, are usually oriented towards technological innovation and financial independence.

Real examples of CBDC

Although CBDCs are still in the early stages, several countries are already actively working on their own versions:

- China. The People’s Bank of China has been testing the e-CNY (digital yuan)for years, one of the most advanced initiatives so far. Several cities are already using it in their local economies.

- Europe. The European Central Bank is exploring the development of a “digital euro”to complement the use of cash and cards.

- United States. Although at a slower pace, the Federal Reserve has shown interest in evaluating the feasibility of a digital dollar.

- Bahamas. The Sand Dollaris a response to the country’s geography, with many islands and remote communities. Its main objective is to improve financial inclusion, allowing the population to have access to banking services and a safe and efficient means of payment, even without a traditional bank account.

- Nigeria. The eNaira was introduced to promote financial inclusion, improve international payments, and reduce cash management costs.

Furthermore, countries like India (e-Rupee), Brazil (Drex) and Sweden (e-krona) are also carrying out studies and pilot tests to implement their own CBDCs in the future.

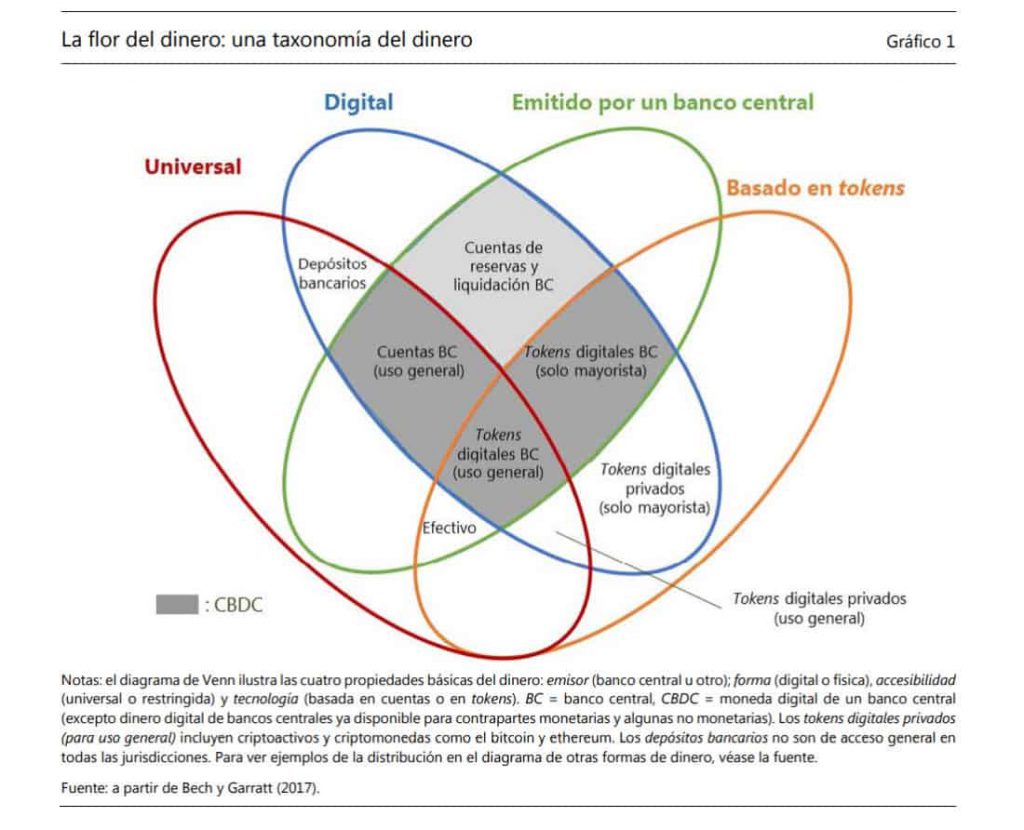

How do CBDCs work?

To function, it uses advanced technologies, such as distributed ledger technology (DLT), which allows secure and fast transactions. These digital currencies are intended for two types of use: for the general public (retail CBDC) and for transactions between large financial institutions (wholesale CBDC).

The main difference between a CBDC and traditional cash is its complete traceability. While a physical bill is anonymous, every transaction with a CBDC leaves a digital trail that the central bank can audit. This gives the State control and complete visibility over the flow of money, which is beneficial for the fight against fraud, but at the same time generates an important debate about user privacy.

Why are central banks launching CBDCs?

Central banks are increasingly interested in CBDCs for several key reasons related to economic efficiency, control over the financial system, and the future of digital money.

For example, CBDCs can make transactions faster, cheaper, and safer. Being digital, transfers between users and between countries could be carried out almost in real time, without the need for costly intermediaries. This could be especially useful for international payments, which often take days and high fees to complete.

On the other hand, the use of cash entails operational costs and security risks, such as theft or counterfeiting. A CBDC would eliminate many of these problems, facilitating the distribution and storage of money. Furthermore, it could be easier to track and prevent the illicit use of money, such as money laundering or the financing of terrorism.

Likewise, in many countries, a significant part of the population still does not have access to traditional banking services. CBDCs could offer a form of financial inclusion, offering a digital currency that citizens could use without needing to have a conventional bank account.

CBDC vs Bitcoin: The clash of philosophies

Although both CBDCs and Bitcoin are forms of digital money that use advanced technologies, their principles and purposes are radically opposite. While a CBDC is your country’s money in digital format, Bitcoin is an alternative financial system that does not depend on any government or central bank. To understand the key differences, here is a direct comparison:

| Characteristic | CBDC | Bitcoin |

| Authority | Centralized | Decentralized |

| Value and Stability | Stable | Volatile |

| Privacy | Traceable | Pseudo-anonymous |

| Purpose | Modernize | Create an alternative and independent financial system from governments and banks |

| Technology | Uses distributed ledger technology (DLT) or blockchain controlled by the issuer. | Uses a public blockchain, without the need for permissions. |

What is the future of CBDCs?

The future of CBDCs is one of the most debated topics in the world of digital finance today. As global economies digitalize at an unprecedented rate, central bank digital currencies are seen as a response to the rise of cryptocurrencies and an opportunity to redefine monetary policy in the digital age.

In fact, global regulators, fintech innovators, and traditional financial institutions are looking at CBDCs as a bridge between the reliability of sovereign currencies and the flexibility of blockchain technology.

Now, the future of CBDCs is advancing rapidly, with pilot projects and developments all over the world, from China to Europe and Latin America. It is expected that by 2030, a significant number of countries will have their own official digital currency.

In this scenario, the relationship with cryptocurrencies will be dual: they could coexist, with CBDCs as official money and cryptocurrencies as investment assets, or compete, as CBDCs could replace the use of stablecoins for certain payments.

To conclude, now that you know the rules of the game, the decision is yours. CBDCs and cryptocurrencies are not just assets, they are philosophies: one offers security and control, while the other bets on autonomy and freedom. In this new financial world, the fear of change and technology is the only enemy.

Choose to understand, choose to learn and take control. You don’t need to be an expert to start, you just need the curiosity to take the first step. The future of money is being written now, and you have the opportunity to be part of it.